Ron, "Cove3", outlining the key factors of the strategic war between Intel and AMD.

Tuesday, January 30, 2007

Friday, January 26, 2007

The 72 Rule

The "72 Rule" allows to approximate the number of periods an investment takes to double the capital with a calculation so simple that you can do it in your head without calculator, and especially without exponentials or logarithms.

This article was inspired by this fragment of a "Fools" analysis, as far as I know this approach is original.

What is it?: If X is the return of an investment expressed in percents, then the number of periods it takes to double the capital is 72/X. For example, if you have a "long" position in an index that averages 7.2% returns per year, then it would take 72/7.2 = 10 years to double your money.

Is it a good approximation? Let's check it with the example.

If the average return is 7.2% per year, then after a year the investment becomes 1.072 what it was. After two years, it is 1.072*1.072 = 1.149184 the initial amount. After 10 years, it would be 1.07210 » 2.0042. So, the approximation wasn't that bad, 10 periods gives a growth very close to exactly double. Conversely, the exact answer would be Log1.072»9.97. In this case the rule gave an approximation within 0.3% of the correct answer.

The problem to calculate the logarithm in the appropriate base is that only scientific calculators have logarithms at all, and it takes too many repeated multiplications to come to an approximation.

Now, let us see how good the approximation is, and how to find an equivalent rule for other objectives, such as thrice the initial investment or 1.5.

Warning: Math comes ahead.

F is the multiplicative factor per period, from the percentage X, it is simply (X/100)+1

The "72 Rule" asserts that F0.72/(F - 1) » 2 ==>

(2Log2 F)0.72/(F - 1) » 2 ==> (Taking logarithm base 2)

Log2 F * 0.72 / (F - 1) » 1

Let us suppose both sides are equal and try to calculate the specific F for which the rule will work exactly, then:

Log2 F = (F - 1)/0.72

This equation holds if F = 1, but reveals what is the trick for values close to 1: To approximate the logarithm base 2 of F with a straight line. Let's see how close that line resembles the log2:

the approximation is good because the line has about the same slope of the logarithm at X = 1 (derivative of Log2(X) = 1/(X*Ln(2)), when X = 1, that becomes 1/ln(2) » 1.44, close enough to 1/0.72 » 1.39. Interestingly enough, they are different!

Let us recapitulate: So far, we could have used any number not 72 to try the same approximation and the logarithm base 2 would have coincided with the straight line at X = 1, but the resulting line wouldn't have been close to the logarithm. By the way, the constant which leads to the tangent at X = 1 would be Ln 2, about 0.69. Thus, if you feel like it, speak of the "69 Rule".

Now, this is a bit of "hairsplitting" because minute variations in the slope of the approximating line become even minuter with small variations around 1, but for curiosity let's see where the 72 leads us:

The slope coincides when

1/(X*Ln(2) = 1/0.72 ==> X = 0.72/Ln(2) » 1.03874.

And Log21.03874 » 0.0548 and (X - 1)/0.72 » 0.0538

We have:

1) Both approximation and log are equal at X = 1

2) The slope on the log was about 1/0.69 > 1/0.72, thus the log grows "faster" at X = 1

3) by X = 1.03874 the log is still above the line but has the same slope

4) We know that the log slope is going to go down, then the curve will bend lower

==>

a) The log will cross again the line.

b) This point (X = 1.03874) is the maximum error in the approximation

This is the moment when you can use your numerical method of choice. I will use a simple graph that says that such thing happens at about 1.078 (no surprise that it is about as far to 1.03874, the max error point, as the max error is to the other solution to the equation, X = 1).

==>

c) This rule works best between 5% and 9%

A bit of worst case: let's say that the returns are 3.9%, the rule says that it takes 72/3.9 periods to double the capital, or 18.46 periods. The Log1.0392 » 18.11, still close enough for practical purposes.

Now you have it, if you want, let's say, to approx the moment of tripling the investment, you can refine this argument and consider that a 100*Ln 3 rule wouldn't be as good as a rule that has an slightly lower slope (higher number of the rule), and you can use the fraction 0.72/0.69 as a guide (115?).

2.3% per period would triple the investment at 115/2.3 = 50 periods according to the "115 Rule" (the correct answer is slightly more than 48.3, 50 is not a bad approx...)

Another consequence of this analysis is that you can use 70 rather than 72 for very small percentages because if you remember, 69 was the slope at 1, thus, for F values much closer to one, 69 is better than 72, but 70 is even easier to remember. For percentages such as monthly returns... Let's say you have 1% per month, the "70 Rule" approximates the number of months to 70. The Log1.012 is 69.66 something, awesome, right?

This article was inspired by this fragment of a "Fools" analysis, as far as I know this approach is original.

What is it?: If X is the return of an investment expressed in percents, then the number of periods it takes to double the capital is 72/X. For example, if you have a "long" position in an index that averages 7.2% returns per year, then it would take 72/7.2 = 10 years to double your money.

Is it a good approximation? Let's check it with the example.

If the average return is 7.2% per year, then after a year the investment becomes 1.072 what it was. After two years, it is 1.072*1.072 = 1.149184 the initial amount. After 10 years, it would be 1.07210 » 2.0042. So, the approximation wasn't that bad, 10 periods gives a growth very close to exactly double. Conversely, the exact answer would be Log1.072»9.97. In this case the rule gave an approximation within 0.3% of the correct answer.

The problem to calculate the logarithm in the appropriate base is that only scientific calculators have logarithms at all, and it takes too many repeated multiplications to come to an approximation.

Now, let us see how good the approximation is, and how to find an equivalent rule for other objectives, such as thrice the initial investment or 1.5.

Warning: Math comes ahead.

F is the multiplicative factor per period, from the percentage X, it is simply (X/100)+1

The "72 Rule" asserts that F0.72/(F - 1) » 2 ==>

(2Log2 F)0.72/(F - 1) » 2 ==> (Taking logarithm base 2)

Log2 F * 0.72 / (F - 1) » 1

Let us suppose both sides are equal and try to calculate the specific F for which the rule will work exactly, then:

Log2 F = (F - 1)/0.72

This equation holds if F = 1, but reveals what is the trick for values close to 1: To approximate the logarithm base 2 of F with a straight line. Let's see how close that line resembles the log2:

the approximation is good because the line has about the same slope of the logarithm at X = 1 (derivative of Log2(X) = 1/(X*Ln(2)), when X = 1, that becomes 1/ln(2) » 1.44, close enough to 1/0.72 » 1.39. Interestingly enough, they are different!

Let us recapitulate: So far, we could have used any number not 72 to try the same approximation and the logarithm base 2 would have coincided with the straight line at X = 1, but the resulting line wouldn't have been close to the logarithm. By the way, the constant which leads to the tangent at X = 1 would be Ln 2, about 0.69. Thus, if you feel like it, speak of the "69 Rule".

Now, this is a bit of "hairsplitting" because minute variations in the slope of the approximating line become even minuter with small variations around 1, but for curiosity let's see where the 72 leads us:

The slope coincides when

1/(X*Ln(2) = 1/0.72 ==> X = 0.72/Ln(2) » 1.03874.

And Log21.03874 » 0.0548 and (X - 1)/0.72 » 0.0538

We have:

1) Both approximation and log are equal at X = 1

2) The slope on the log was about 1/0.69 > 1/0.72, thus the log grows "faster" at X = 1

3) by X = 1.03874 the log is still above the line but has the same slope

4) We know that the log slope is going to go down, then the curve will bend lower

==>

a) The log will cross again the line.

b) This point (X = 1.03874) is the maximum error in the approximation

This is the moment when you can use your numerical method of choice. I will use a simple graph that says that such thing happens at about 1.078 (no surprise that it is about as far to 1.03874, the max error point, as the max error is to the other solution to the equation, X = 1).

==>

c) This rule works best between 5% and 9%

A bit of worst case: let's say that the returns are 3.9%, the rule says that it takes 72/3.9 periods to double the capital, or 18.46 periods. The Log1.0392 » 18.11, still close enough for practical purposes.

Now you have it, if you want, let's say, to approx the moment of tripling the investment, you can refine this argument and consider that a 100*Ln 3 rule wouldn't be as good as a rule that has an slightly lower slope (higher number of the rule), and you can use the fraction 0.72/0.69 as a guide (115?).

2.3% per period would triple the investment at 115/2.3 = 50 periods according to the "115 Rule" (the correct answer is slightly more than 48.3, 50 is not a bad approx...)

Another consequence of this analysis is that you can use 70 rather than 72 for very small percentages because if you remember, 69 was the slope at 1, thus, for F values much closer to one, 69 is better than 72, but 70 is even easier to remember. For percentages such as monthly returns... Let's say you have 1% per month, the "70 Rule" approximates the number of months to 70. The Log1.012 is 69.66 something, awesome, right?

Saturday, January 20, 2007

The Sandwich

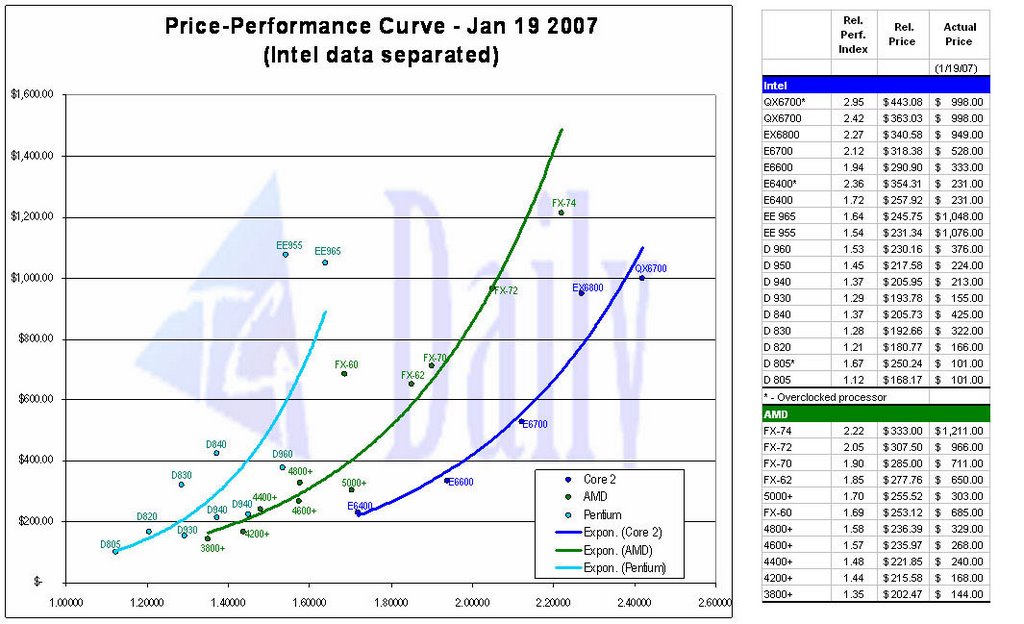

Thanks to Tom's Hardware Guide for this magnificent updated graph:

This graphic has some controversy about the performance measurements, but for the most part, the trends are there. Yes, I have come to validate the notion that Core 2 Duos are quite simply superior to anything AMD produces, with the only possible exception of the entry level dual cores 3600+ X2 at 65nm which is "Energy Efficient" and the 3800+ X2 because they have better performance/(power*price).

In this graphic you can not completely see how bad the Pentium processors are, because their inefficient power consumption is not part of the performance data.

But in any case, you may see here that the only competitively priced AMD processor is the 5000+ X2, and that barely.

Although the gist of the article in which this graphic appears is that AMD is raising its prices, you can see that such initiative wouldn't fly much. Whoever has the money to buy products mentioned in this chart goes to sites like THG for guidance, and the community of benchmarkers pretty much agree with THG, furthermore, Core 2 Duos have positive rapport among customers.

Perhaps AMD is relenting in its insistence to win market share. We have seen this year how inelastic the demand for processors is, thus, there is simply more money to be made raising the prices, if the market share losses are moderate. Why would AMD do that? because it needs money, perhaps to compensate for the huge ATI losses that must be occurring now. If AMD keeps being optimistic about ATI they may say that right now it is more important to have better cash flows than to gain market share, so that the company may finance the projects that will enable better products to make another market share win charge.

Continuing with "AMD's long year", I said that "AMD is losing lots of revenue share between the ceiling that superior Intel products impose and over the quicksand created by millions upon millions of netbusteds" are being dumped, that is the sandwich that this graphic illustrates.

Inelastic: Let us suppose that you have a retail store and product X costs almost nothing to you. You obviously want to make the most money with X, either selling small numbers at a high price, large numbers at low price, or something in between. The answer depends on the demand elasticity of X. If you lower the price of X 1% and that stimulates demand to raise 1% then X would be said to have 1 of demand elasticity coefficient. If you lower X price 1% but see that demands increases 2%, then you would try to lower the price as much as possible because the increase in demand is overcompensated by what you are not receiving in price per unit. If you lower prices 2% but only see 1% inrease in demand, then X is called "inelastic". In this case, you win more money if you raise prices as much as you can. The problem with raising prices, naturally, is that your customers go to your competition. The market share shifting tells you how far you can go.

Wednesday, January 17, 2007

A long year for AMD

AMD couldn't make it this quarter, which is the most important in the year, because it grew revenues merely 3% sequentially while Intel grew 8% when usually the jump due to the holiday season is more than 10%.

I am very surprised that AMD said that it blew the most important quarter in what profiles to be a horrible year and the beating didn't go much further than $18, furthermore there was AMD trading upwards of 110 million shares, the most ever. The ~$17.95 price level of that day constitutes hard support with the information we know, but there remains important incognitas to be cleared, thus $18 may seem a good price to short-sell AMD after all (1).

This is what happens:

There were high hopes for a Vista-induced recovery early in the year, but the cards have been dealt and we know that is not happening, only a slow improvement in demand. This is important also because the digital TV side was the part that could have benefited most.

Anyway, this year is going to be governed by the issues raised at the ATI purchase, thus I will begin the analysis there.

ATI as a standalone company was valued at X because it was a business capable of generating Y revenues and Z profits(/losses). What is valuable about ATI isn't their offices or inventories of product, but the designs that may be turned into products, the established distribution channels, the experience to deal with the technology issues, and so on. I would call this the ATI "softcapital".

To purchase ATI, AMD had to pay the usual 20% premium that happens in these cases. Nevertheless, inside AMD, ATI is not a business capable of Y revenues nor Z profits, but, for simplicity's sake, Y/2 revenues and substantial losses; because more than half of the market for ATI products are Intel based computers that won't exists because Intel and ATI won't cooperate further to integrate their designs, and Intel will give preferential treatment to nVidia, which is the graphics technology leader, anyway. Thus, by just purchasing ATI, AMD devalued it significantly, let's say to a half. Then, AMD paid 120% for a business that inside it is worth half... 240% of what the market values that business. You may disagree with these numbers, but that is not important, what is important is that inside AMD, ATI is worth much less than standalone. This should have been a decisive deterrent for a purchase, but nevertheless, AMD went ahead with it.

Did AMD have projects to invest in? Yes, it has: A New York Fab, more production facilities at Dresden, and conversion of Fab30.

Isn't another loss the forced allienation of nVidia, whoose 3d graphics designs are superior to ATI's and also has a quite competitive business in chipsets?

On the other hand, AMD has still to pay huge charges due to the restructuring of the resulting company and to service the huge debt it incurred to purchase ATI. This means that just to break even, AMD must find not just synergies and leveraging opportunities for the ATI side of the business that may compensate the acquisition related charges and its debt financing, but also the devaluation of the ATI business, the missed benefits of other projects, and the cooling down of partnerships with nVidia.

Thanks to this approach I finally got to a definitive conclusion: Purchasing ATI was a blunder.

If it was going to devalue ATI so much, I would have preferred to go on the slow (but sure) path of partnership to develop Fusion and other initiatives. My opinion is that an ATI purchase was not a requisite for a 2009 schedule of MCM processors with graphic capabilities (fusion), and this approach had the important benefit of being able to invite nVidia in. Instead, AMD changed its focus from enthusing the partners about more accessible short-medium term initiatives such as Torrenza graphics and physics coprocessors for a very distant fusion initiative, leaving orphaned initiatives such as 4x4 that without coprocessors seem ill-conceived (2).

Those $500 million acquisition related charges translates to about $0.9 per share, that is, they wipe out the prognosticated earnings of a whole year!.

The only initiatives that AMD is pursuing are production capacity expansion and fusion. But we know that the market already has plenty of production capacity, that AMD really doesn't have competitive advantages here; and we know that fusion is very far and may become an irrelevant success if AMD loses continously revenue share, market share, and mindshare for the next two years, just as AMD64 was an out-of-this-world advantage that could only be made use of to penetrate a rather small portion of the server market before Intel, for all practical purposes, catched up.

And AMD is losing lots of revenue share between the ceiling that superior Intel products impose and over the quicksand created by millions upon millions of netbusteds.

There could be hope if the introduction of the 65nm processors would have shown 1) A truly mature process, 2) Performance advantages. Nevertheless, the current 65nm shrink effectively turned out equivalent to a 75nm shrink without performance advantages, rather, minor performance disadvantages, only improved power efficiency. This is every bit as worrysome as the faith some AMD bulls have in the quadcores, because the exponential nature of the worsening of yields mean that there is no chance for AMD to produce single die quadcores if its yields are not fantastic ~95% in equivalent single cores, and not having been able to shrink to sub-70nm effective feature sizes mean that the process is not mature, and it is becoming late in the game for the quaddies when Intel's double duals are already performing well in the market and by the time AMD manages to introduce them Intel may be on the market with 45nm products.

Thus, we may conclude that ATI will "provide" losses rather than synergies to compensate for the huge financial and other kinds of burdens it is imposing on AMD, while Intel is swamping the market with superior products and firesaling netbusteds; and there is the possibility that AMD is stalling at 65nm inducing delays in quadcores, the only products of interest in its roadmap.

Notes:

1)I am not advocating to short sell AMD, just explaining that the the price may crash despite the huge trading that happened at the upper $17 level

2)The difference between a dual socket workstation/server and a dual socket gaming computer is small: The server requires higher reliability and expandability, hence the registered dimms, but the gaming station may work with the cheapest hardware available, hence the unbuffered dimms. The other part of 4x4 is to have huge I/O capabilities, but not for network or storage as a server, but for graphics. That's why it is to be expected that 4x4 motherboards will have double everything. In the 4x4 architecture, only one of the sockets has access to I/O, which bears the quesiton why: That way the computer may work with only one processor. This bears another question: If one processor is enough for the huge graphic I/O of 4x4, then what is the point of the dual socket? -- Artificial Intelligence, Physics, or Graphics coprocessors!. In the absence of coprocessors, all you can do is to put another processor, further erasing differences with a workstation. That's why 4x4 seems so silly.

Subscribe to:

Posts (Atom)